PIP-72 - Liquidity Funding for Futarchy Experimentation in Velora Governance

Co-authors: Velora Growth Committee & Futarchy.fi

⸻

Abstract

If approved, this proposal will:

• Launch a non-binding futarchy pilot with Futarchy.fi to test futarchy evaluations (YES/NO conditional markets) in Velora governance.

• Enable the Velora Growth Committee to create markets forecasting VLR price outcomes of proposals and milestones.

• Deploy $50,000 in DAO liquidity (25,000 VLR + 25,000 sDAI) into Uniswap V3; funds return to the treasury after the trial.

• Require no operational budget, only temporary liquidity, with minimal impermanent loss (≤ $1.5k for 50% $VLR price increase).

• Explore a potential Velora integration in Futarchy.fi, opening the door for deeper protocol partnerships.

• Establish an advisory evaluation mechanism: after a 7-day window, compute an impact estimate (YES–NO TWAP); recommend For if ≥ +1%, Against if ≤ −1%, and Neutral otherwise.

⸻

Goals & Review

With the Road to Velora campaign progressing and the $VLR migration in progress, this is a timely moment to test new governance tools.

The pilot is non-binding: futarchy evaluations will not trigger on-chain actions, but will provide signals on proposals and milestones that may help delegates and contributors gauge sentiment, timing, or traction.

If successful, this experiment could:

• Encourage richer discussion.

• Validate futarchy as a governance signal.

• Open the door to formal integrations of futarchy-style tools into Velora governance.

See: From Signals to Systems.

Pilot Objectives

• Test a new governance tool

• Run a low-risk futarchy experiment that generates decision-making signals without altering existing DAO processes.

• Explore infrastructure integration

• Showcase Futarchy.fi and Seer One’s interest in integrating Velora routing, and test how this could support their operational needs.

• Boost community engagement

• Highlight Velora’s rebrand and token migration, while encouraging wider participation.

⸻

Scope & Means

Liquidity Deployment

- The pilot will deploy $50,000 USD in liquidity (25,000 USD in VLR and 25,000 USD in stables) using Uniswap v3 on Ethereum Mainnet under the following parameters:

• Contract: Uniswap v3 (full-range) on Ethereum Mainnet, fee tier 0.01%.

• Concentration: By default, liquidity is deployed in a wide (“baseline”) range. Optionally, the multisig may deploy up to 5× concentrated liquidity (narrower tick ranges) per market to improve price discovery and slippage near the current price.

• Full-range Liquidity: At least 20% of the capital allocated to each pool will be deployed in a full-range position to ensure price discovery during volatility.

• Arbitrage: Up to 5% of the capital may be allocated to arbitrage contracts, which will arbitrage between spot and conditional markets. Arbitrage profits belong to the DAO and may be reused as liquidity.

• Rebalancing: For concentrated liquidity positions, rebalancing may be performed at most once per 24h.

Market Setup

Markets will be organized around two primary categories: Milestone-Based Markets and Governance Proposal Markets. As of now, token price is the one core metric that can be considered within Futarchy.fi. In the future, other metrics may become available, but we believe token price represents a good starting point for evaluating the expected impact of major events.

Milestone-Based Markets

These markets explore how events like token migrations, integrations, or campaign outcomes might affect protocol metrics. Examples include:

• What will VLR’s price be if Velora’s average monthly trading volume exceeds $X million during Q4 2025?

→ Shows whether traders think more trading activity will actually push VLR’s price up.

• What will VLR’s price be if Velora’s cumulative protocol revenue surpasses $Y during Q4 2025?

→ Checks if the market expects higher revenue to have a direct effect on VLR’s price.

Other DAOs are already testing similar designs. For example:

• What will be the impact on GNO price if Circle deploys native USDC on Gnosis Chain on/or before December 31, 2025? - See market

Governance Proposal Markets

These markets estimate the anticipated effect of governance proposals on one or more protocol metrics.

• Example: What will be the impact on $GNO price if GIP128 is approved? - See market

• In Velora, a relevant case is PIP-59 (Proposal for Returning 40.203 wETH to Bybit), which prompted a strong debate. A futarchy market tied to VLR price or protocol volume could have offered additional insight for tokenholders focused on outcomes beyond sentiment or principle, especially in controversial decisions.

Evaluation Rule

Each futarchy evaluation will run for 7 days, during which liquidity remains active in the markets. To guarantee reliable price signals, at least 20% of every pool will always be kept in full-range positions, ensuring continuous TWAP calculations even during volatility.

At the end of the evaluation window, the estimated impact is calculated as the difference between the TWAP of the YES market and the TWAP of the NO market. Based on this outcome, the pilot will issue an advisory recommendation:

• For if the impact (YES − NO) ≥ +1%

• Against if the impact ≤ −1%

• Neutral otherwise

To avoid spreading liquidity too thin, the pilot will evaluate only one governance proposal at a time, alongside at most three milestone markets in parallel.

Multisig

• Create 2-of-3 multisig (2 DAO Members (GTF + VGC member or Laita) + Futarchy.fi). A member of futarchy.fi is required for organizational purposes.

• Powers: deploy liquidity, rebalance (≤1/day), allocate ≤5% to arbitrage.

• All activity displayed on the DAO forum.

Community Participation

• Open Access: All markets will be open to anyone: traders, liquidity providers, and curious DAO members with no technical or eligibility barriers.

• Transparent Data: All trading, pricing, and market resolution data will be publicly available and on-chain.

• Education & Onboarding:

- VGC & Futarchy.fi will co-host a community call to introduce the pilot and explain how each futarchy evaluation works.

- The VGC will produce and publish educational content explaining how futarchy works, what the pilot aims to test, and how participants can get involved.

⸻

Implementation Overview

Time of Implementation

• Immediate after proposal passes.

Duration

• 6-month trial period.

• DAO may terminate early via Snapshot vote.

Steps

- Create multisig.

- Transfer VLR and/or DAO assets from the main treasury to multisig (or equivalent VLR/wETH swapped to stables if unavailable).

- Launch markets (proposals & milestones).

- Manage Uniswap v3 positions per the Liquidity Mandate (≥20% full-range, ≤5× concentration, ≤1 rebalance/day).

- Resolve markets via Reality.eth & Kleros Oracle.

- Publish post-pilot review including participation, volume, impermanent loss and accuracy of Futarchy signals.

⸻

Post-Pilot Review

• VGC & Futarchy.fi to deliver assessment covering:

• Outcomes.

• Participation.

• Insights for next steps.

⸻

Budget & Cost

This proposal does not request an operational budget, it only asks the DAO to provide liquidity to seed the pilot markets.

• Liquidity Provision: $50,000 (25,000 VLR + 25,000 sDAI).

The DAO’s risk exposure from liquidity provision is minimal. Based on simulations with $25,000 VLR + $25,000 sDAI, impermanent loss is <= 2% of deployed liquidity under a 50% price move, and lower for smaller moves.

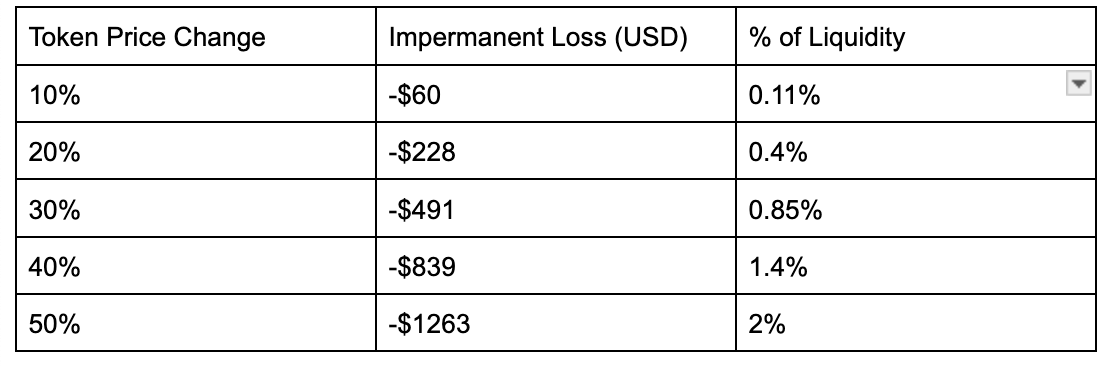

Impermanent Loss Analysis (Full-Range Liquidity)

Token Price Change IL (USD) % of Liquidity

Even in the unlikely event of a 50% VLR price swing during the pilot, the DAO’s maximum IL exposure would be less than $1.5k for a full-range liquidity position For more moderate movements (10–30%), IL is negligible.

In other words: the DAO’s cost exposure is small, predictable, and primarily a function of VLR price movement during each market.

For concentrated liquidity (up to 5× narrower), impermanent loss can be higher, but rebalancing is capped at once per 24h. At least 20% of liquidity is always kept full-range, which ensures continuous pricing and limits downside exposure.

⸻

Why Futarchy.fi?

Futarchy.fi is the first Ethereum-native platform designed specifically for running futarchy evaluations with conditional markets, putting Robin Hanson’s idea of “vote on values, bet on beliefs” into practice. Built on the battle-tested Gnosis Conditional Token Framework, the platform uses conditional outcome tokens and resolves markets through Reality.eth and Kleros, a decentralized oracle and arbitration stack.

The Futarchy.fi platform is already being tested by different DAOs, for VeloraDAO, it offers a clear and flexible way to experiment with conditional-market-driven governance.

Opportunity for Velora

Foster Opportunity for Velora Integration

Futarchy.fi could benefit from an intent-based protocol like Velora, to optimize the routing of orders and swaps. A first step would be a joint exploration with the VGC if this pilot is approved.

In the long run, such an integration would allow Velora DAO to use the same liquidity provided for futarchy markets as regular VLR liquidity. In practice, this means that if someone swaps between VLR and sDAI, their trade could be routed through the YES VLR and NO VLR pools, so the liquidity serves both futarchy evaluations (YES/NO conditional markets) and everyday trading at the same time.

This would enable the same LP to be used for two purposes:

- Futarchy Markets

- Regular Liquidity between VLR and sDAI

⸻

Risks & Mitigations

• Financial Risk: limited to impermanent loss.

• Operational Risk: multisig ensures controlled deployment; rules cap rebalancing and IL exposure.

• Adoption Risk: pilot is advisory, non-binding; no protocol actions depend on it.

⸻

Voting Options

• Option A: Approve $50,000 liquidity (25,000 USD in VLR + 25,000 sDAI) for 6-month futarchy pilot.

• Option B: Do not provide liquidity.

• Option C: Abstain.

Useful links

- Futarchy.fi - https://docs.futarchy.fi

- Vote Values, But Bet Beliefs - Futarchy: Vote Values, But Bet Beliefs

- Futarchy Website/Trade - Futarchy.fi - Markets Know Better Than Experts

- Seer.pm - https://app.seer.pm/

- Reality.eth - Reality.eth — reality.eth documentation

- Kleros - https://kleros.io/

- DAPPCON 2025: Launching Futarchy: Conditional Spot Markets for GnosisDAO and Beyond - https://www.youtube.com/watch?v=N-wc59t44iE

- Futarchy: Decentralizing Decision-Making with Market-Driven Governance - https://www.youtube.com/watch?v=oo7irCsoNmA