Background

Velora rebranded from ParaSwap, introducing a major shift in positioning and functionality. Alongside this transition, the PSP token was migrated 1:1 into the new VLR token, which now underpins governance, staking, and ecosystem alignment.

With the rebrand, Velora moved beyond its role as a DEX aggregator to adopt an intent-based, cross-chain trading architecture, enabling improved execution, MEV protection, and broader ecosystem integrations.

Velora Performance

Following migration incentives and promotional campaigns, trading activity and volume have seen measurable growth, with PSP holders actively participating in the new Velora.

-

Trading volume: In the past 30 days, Velora has processed $100M–$300M per day on average, with spikes above $820M. Cumulative trading volume surpassed $7B in September, boasting approximately $133B lifetime volume, which places Velora among the top DEX aggregators.

-

Revenue: YTD protocol revenue is tracking at around $3.4M, with $741.6K earned in the last 90 days from trading fees. Revenue by epoch is volatile, peaking above $596K in an epoch. Recent epochs continue to deliver between $150K–200K. In general,

-

Staking seVLR: Staking TVL sits at $4.3M, with 298.3M VLR staked by 635 unique stakers.

Data from https://dashboard.velora.xyz/public/dashboard/

Legacy Revenue-Sharing Models

Under PSP / PSP 2.0, 80% of protocol revenue was distributed to stakers in ETH (mostly via sePSP2).

That created strong direct incentives for stakers, but it also introduced structural problems: limited treasury flexibility, weak direct demand for the token (since revenue is paid in ETH), and scaling friction for growth investments.

Below unpacking the pros and cons of the current seVLR revenue-sharing model

- Pros:

- Token stakers receive a clear, recurring economic benefit tied to protocol performance.

- seVLR encourages protocol participation (liquidity, governance, actions).

- Distributing revenue visibly shows revenues are real and flowing to users.

- Cons:

- Weak linkage to protocol performance value:

80% of protocol revenue is shared with stakers. This design mainly rewards holding rather than creating organic demand for PSP. Revenue growth benefits existing stakers, but it doesn’t inherently drive new token purchases or strengthen long-term price support.

- Treasury, reinvestment, and liquidity limitations

Allocating 80% of revenue directly to payouts leaves the DAO with minimal runway to invest in critical areas such as R&D, security, marketing, ecosystem incentives, and opportunistic growth. In periods of market stress, the DAO lacks the financial buffers to maintain incentives or absorb unexpected costs.

- Operational friction & costs

Distributing ETH on Ethereum periodically is gas-heavy and costly to execute at scale. Converting heterogeneous fee flows into ETH requires swaps, slippage, and accounting complexity.

- Accessibility & complexity

The sePSP model and fee-sharing mechanics are harder for casual users to understand and adopt, limiting broad participation.

- Scalability and liquidity constraints

The legacy revenue-sharing model restricts the DAO from seeding liquidity on other networks (e.g., Base), limiting its capacity to expand reach, sustain market depth, and remain competitive across ecosystems.

A rigid high revenue share to stakers is hard to scale as the protocol expands across chains. Lack of other distribution avenues beyond just incentives also gives less incentives for ‘early’ stakers, versus also supplementing it with token rewards.

A Buyback Mechanism for Velora

Industrial Examples

1. Hyperliquid

Hyperliquid has built one of the most aggressive buyback-and-burn mechanisms in DeFi. The protocol directs nearly all trading fees into its Assistance Fund (AF), which automatically recycles revenue into daily HYPE buybacks on the native HYPE/USDC order book.

Structure & Execution

- Revenue source: Trading fees collected across HyperCore and HyperEVM

- Buyback: ~$3–3.5M in HYPE purchases per day (~63K HYPE). ~$23M in weekly buybacks, directly proportional to fee revenue.

- Burn mechanism: A portion of purchased HYPE is sent to a burn address, permanently reducing supply.

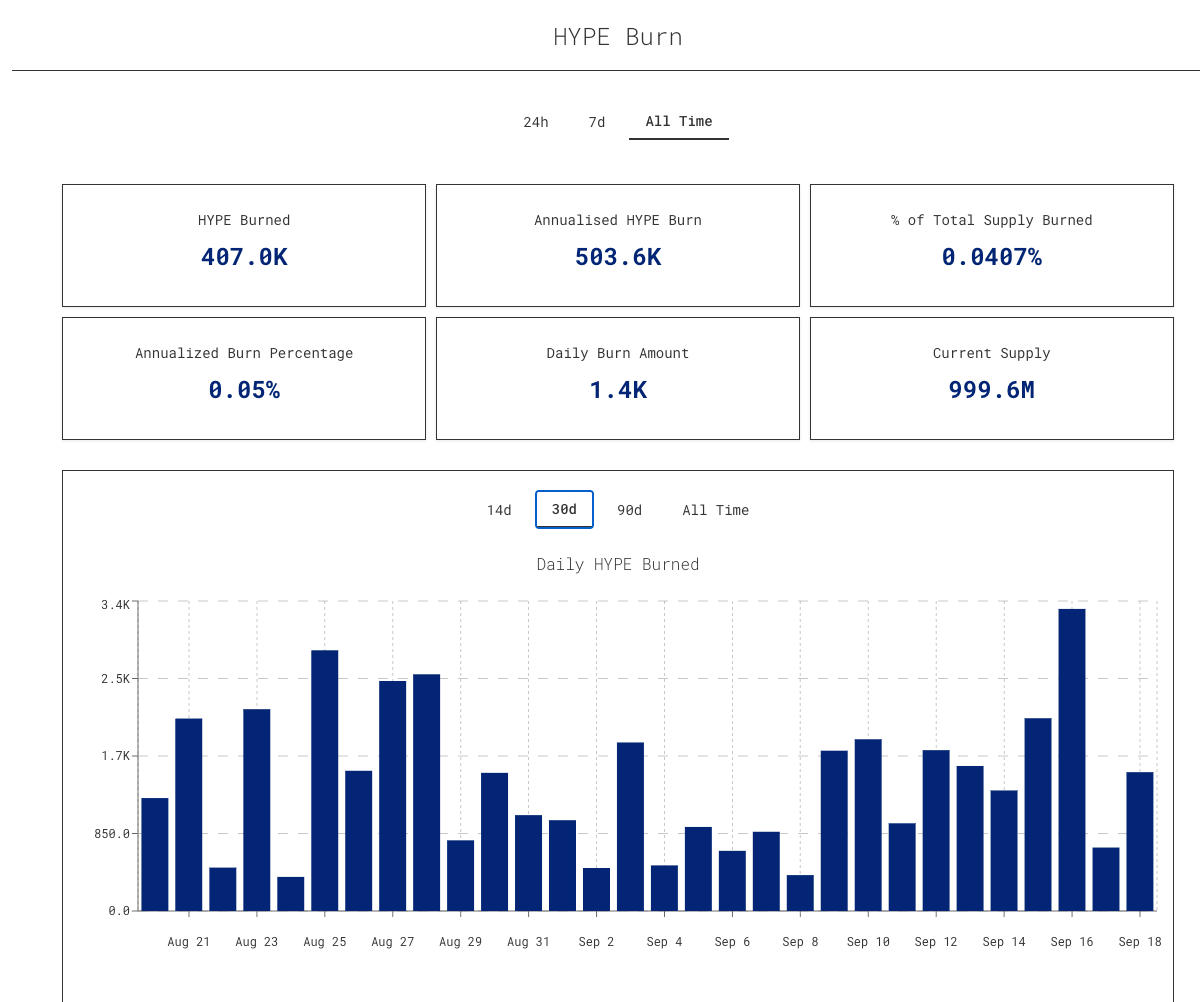

Impact & Results (as of September 2025)

- In the past 30 days, HyperCore has generated revenue exceeding $110.3M. AF has spent over $100.57M on HYPE buybacks, acquiring around 2.13M HYPE at an average price of $47.90.

- On a daily basis, this equates to roughly $3–3.5M in HYPE bought per day (~63K tokens daily).

- Over a 7-day window, the fund consistently absorbs over $23M of supply, showing the system’s throughput is directly tied to trading volume and fee generation.

From late 2024 to September 2025, Hyperliquid has permanently burnt over 409.9K HYPE (~0.041% of supply), at a rate of ~1.4K HYPE (~$82,000) per day. The annualized burn amount rate is around 0.05%.

The effect is a powerful flywheel: higher trading activity generates more fees, which drive larger buybacks, while steady burns enforce long-term scarcity. As a result, Hyperliquid’s HYPE token has appreciated from ~$15 in March 2025 to ~$58 by mid-September 2025, with the AF acting as a constant source of buy pressure in the market.

2. Aave

On April 9, 2025, Aave DAO approved a $1 million weekly token buyback initiative with overwhelming support, 439,000 votes in favor vs 2,020 against. This initiative was launched in response to a ~21% decline in AAVE’s market value (trading around $120 at the time) and aims to reinforce tokenomics and long-term incentive alignment.

Structure & Execution

- Initial Allocation: $4 million for the first month.

- Ongoing Commitment: Up to $1 million worth of AAVE repurchased weekly for six months.

- The six-month timeline can be extended by governance if results prove favorable, as seen in past programs like Merit.

Impact & Results (as of September 17, 2025)

- Total buyback: 87,894 AAVE (~0.5% of total supply)

- Total spend: $21.05 million

- Profit: $4.93 million

- Emissions are reduced by 50%, strengthening AAVE’s tokenomics. Onchain data shows increased accumulation and reduced sell pressure. Positive price and TVL trends observed since the buyback began.

To build on the momentum of the current program, the DAO could consider making buybacks a permanent fixture at or near current levels ($500K–$1M per week). Regular buybacks would reinforce market confidence in AAVE, ensure protocol revenues flow back to tokenholders, and provide a stable foundation for long-term tokenomics.

3. Sky Ecosystem

In 2024, MakerDAO rebranded as the Sky Ecosystem and migrated its governance token from MKR to SKY at a fixed rate of 1 MKR = 24,000 SKY. The protocol continues the Smart Burn Engine (SBE), an automated mechanism that ties protocol revenues directly to SKY buybacks and burns.

Structure & Execution

- Revenue source: Stability fees and real-world asset yields flow into the Surplus Buffer (USDS).

- Trigger: Once the buffer exceeds the activation threshold (1M USDS, vow.hump), the Surplus Buffer Splitter (SBE) deploys fixed increments (10k USDS, vow.bump) every ~36 minutes (splitter.hop).

- Allocation: Each increment is divided into three streams:

- 25% → SKY accumulation (held by the protocol treasury)

- 75% → SKY staking rewards (distributed to stakers).

- Burn rule: 25% of each vow.bump (2,500 USDS) is routed to the legacy Flapper contract, which swaps USDS for SKY on the open market and burns it.

- Daily Quotas: Governance requires the Splitter to guarantee 100k USDS/day of SKY buybacks and 300k USDS/day of SKY staking rewards. If normal flows fall short, parameters adjust to meet these minimums.

Impact & Results (as of September 2025)

- Total Spent: ~$76.5M USDS

- Total SKY buyback & burned: ~1.193B SKY (~4.2% of supply)

- Average buyback price: $0.0641 SKY/USDS.

- Daily Buyback/Burn: 1–3M SKY (~$70–100k notional).

- Treasury performance: ~17.25% gains on past purchases.

SKY has traded between $0.037 and $0.094 over the year, and the program has proven profitable: the treasury shows ~17.25% gains on past purchases, reinforcing the reflexive cycle where protocol growth → surplus expansion → larger buybacks → stronger token value.

Our suggestion

As the protocol continues to mature, we are now opening a community discussion on introducing a token buyback program with multiple approaches for governance to consider.

We suggest initiating the buyback of VLR in the open market. The purchased VLR will be used to build the protocol treasury, distribute to seVLR stakers, and seed liquidity on supporting DEXs to increase TVL onchain for VLR.

The model will create a self-reinforcing loop:

Product improvements & incentives → Higher trading volume & integrations → Revenue growth → Stronger token demand/price via buybacks → More protocol adoption & mindshare → Further trading volume growth → More revenue

- Buybacks create direct demand for VLR, potentially supporting price stability in weaker markets.

- Buybacks signal strong fundamentals and increase confidence among token holders and DAO.

- Buybacks balance between reinvestment in growth and direct returns to token holders.

- As Velora expands multi-chain, a structured buyback program can strengthen its reputation as a sustainable and community-aligned DeFi protocol.

If Velora introduced a token buyback, it would become the first cross-chain intent-based trading aggregator to execute a token buyback mechanism.

Key Considerations

1. VLR Treasury

Preserving a strong treasury from token buyback is essential for Velora’s resilience and long-term positioning. A well-funded treasury allows the protocol to:

-

Sustain growth and operations during market downturns.

-

Finance ecosystem partnerships, integrations, and security providers.

-

Maintain flexibility to capitalize on strategic opportunities as they arise.

2. Burning vs Non-Burning

During Velora’s growth phase, we see merit in not burning purchased VLR immediately, instead recycling them into incentives and liquidity programs. This facilitates token movement from weak hands to aligned partners while mitigating opportunity cost.

In the longer term, once Velora enters a more mature growth stage, burning may become preferable to reduce supply and entrench value accrual.

Conclusion

This research aims to open a discussion on whether and how Velora should introduce a VLR token buyback mechanism.

By weighing the trade-offs and opportunities, Velora DAO can develop a strategy that supports both Velora’s long-term growth and tokenholder value.

We appreciate your feedback on this matter.